-

-

CIO INSIGHTS

-

BACK TO CIO INSIGHTS

BACK TO ARTICLES & INSIGHTS HOME

BACK TO CIO INSIGHTS

BACK TO ARTICLES & INSIGHTS HOME

-

-

-

![Michael Rosen]()

-

Investment Insights are written by Angeles' CIO Michael Rosen

Michael has more than 30 years experience as an institutional portfolio manager, investment strategist, trader and academic.

VALUATION

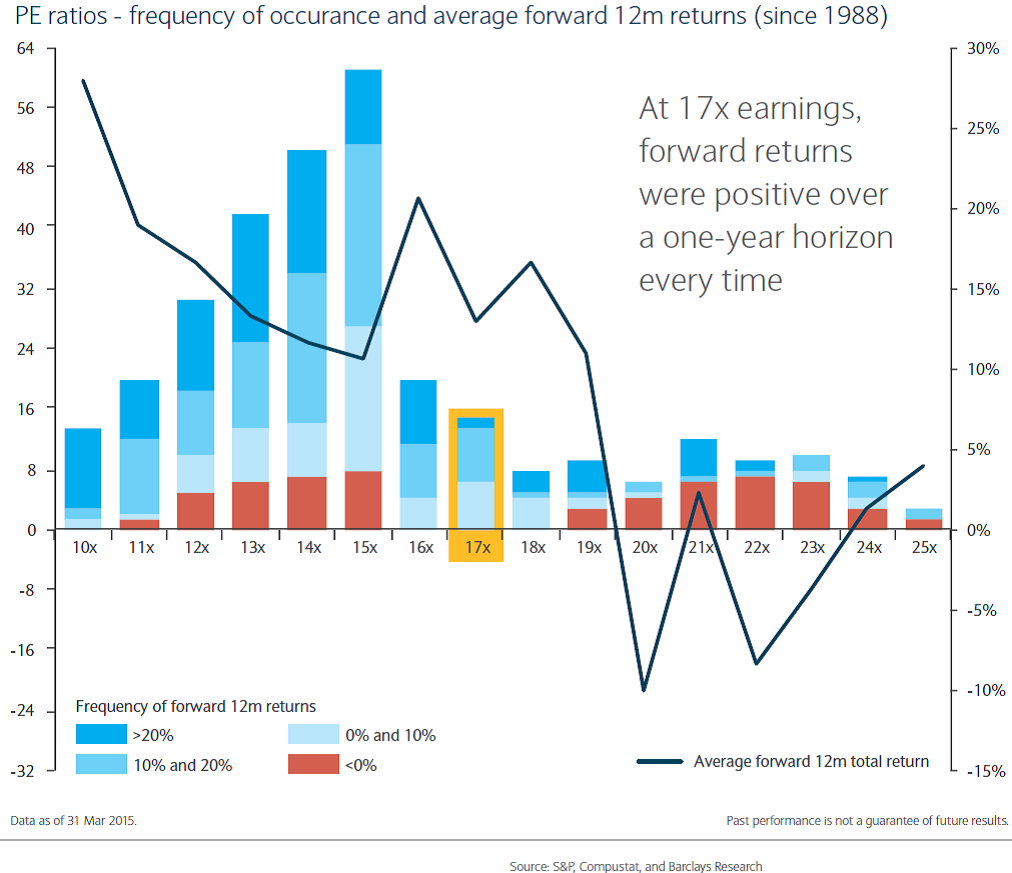

Published: 04-21-2015Most observers would agree that equities are rich (expensive, overpriced, etc.). Corporate profits are at record highs, and the forward price-to-(optimistic) earnings multiple on the S&P 500, at 17x, is the highest since 2004.

A favorite counterargument is a relative one: stocks may be expensive, but bonds are way more overvalued. With a 2% yield, the 10-year Treasury has a P/E multiple of 50x (taking the inverse of its yield). Of course, German bunds have an infinite P/E (with its negative yield). So stocks are the cheapest house in an expensive neighborhood.

That may be true, but this counterargument isn’t really a “counter,” i.e., stocks could still be expensive on their own even if other asset classes are more expensive.

The chart below (courtesy Barclays) shows the number of monthly observations of the S&P 500 at various forward P/E multiples (left y-axis). The subsequent average 12-month return is depicted by the black line (scaled to the right y-axis). And the range of subsequent 12-month returns at each P/E multiple is shown by the colors of each bar.

I like charts that convey a lot of information simultaneously (as this does), and this one leads me to three observations. The first two are pretty obvious/intuitive, the third, a bit more interesting:

- average future returns are higher when multiples are cheap than when multiples are expensive;

- negative forward returns can occur from both cheap and expensive multiples, although are more common when starting from an expensive base;

- forward returns have always been positive when multiples are in the middle range of valuation (as we are now).

I have not seen a rigorous study to explain this third point, but I’d speculate that the middle ground of valuation reflects an equilibrium environment that balances the macroeconomic risks of growth and inflation.

Of course, no law governs this observation, and the future path of equity prices is unknown. But in weighing the evidence, I see no compelling reason to deviate from our long-term strategy.

PRINT THIS ARTICLE

-

![Beach Reading]()

Beach Reading 08-10-2023

There's still a lot of summer left, so I have five nonfiction and five fiction recommendations for your beach ...

READ BLOG POST -

![Wild, Wild East]()

Wild, Wild East 07-13-2015

The central planners in Beijing have gotten so much right for the past three decades, that they might be forgiven for ...

READ BLOG POST -

![Yellow Flag]()

Yellow Flag 05-10-2022

When cars crash in an auto race, the yellow flag comes out. This requires drivers to slow down and stay in their ...

READ BLOG POST

-

-

CONNECT WITH USSUBSCRIBE TO ANGELES' INSIGHTS

Get the latest investment information and stay on top of market trends.

SUBSCRIBE -

CONTACT US

![Location: Los Angeles]()

SANTA MONICA

429 SANTA MONICA BLVD

SUITE 650

SANTA MONICA, CA 90401

310.393.6300

GET DIRECTIONS -

![Location: New York]()

NEW YORK

375 PARK AVENUE

SUITE 2209

NEW YORK, NY 10152

212.451.9240

GET DIRECTIONS -

![Location: Houston]()

HOUSTON

5151 SAN FELIPE ST

SUITE 1480

HOUSTON, TX 77056

713.832.3670

GET DIRECTIONS